What is wealth tax?

Vous l’avez peut-être déjà entendu, mais pour rappel la Suisse reste l’un des rares pays à prévoir un impôt sur la fortune. L’impôt sur la fortune est un impôt complémentaire à l’impôt sur le revenu. L’impôt sur la fortune n’est pas prélevé par la Confédération.

In addition to its contribution in terms of tax revenue, wealth tax is also a control tax.

By monitoring changes in the taxpayer's assets over time, the tax authorities are able to check that income has been declared correctly.

Items subject to wealth tax

The taxpayer's wealth is broadly defined. It includes all movable and immovable property. The following in particular are subject to wealth tax:

- Les immeubles

- les actions, obligations et valeurs mobilières de toute nature, mises de fonds, apports et commandites représentant une part d'intérêt dans une entreprise, une société ou une association

- L'argent comptant, les dépôts dans les banques et caisses d'épargne, les soldes de comptes courants et tous titres représentant la possession d'une somme d'argent

- Les parts de placements collectifs qui possèdent des immeubles en propriété directe, pour la différence entre la valeur de l’ensemble des actifs du placement et celle de ses immeubles en propriété directe

- Les créances hypothécaires et chirographaires

- Les éléments composant la fortune commerciale

- Les assurances-vie et vieillesse pour leur valeur de rachat

- Les bijoux et l'argenterie, lorsque leur valeur dépasse 2'000 CHF

- Le cheptel, tant mort que vif

Items exempt from wealth tax

- Les meubles, y compris les collections artistiques et scientifiques qui peuvent être considérées comme telles

- Les vêtements

- Les ustensiles de ménage

- Les livres servant à l'usage du contribuable et de sa famille

- Le capital versé à titre d'épargne (LPP)

Determining gross and net assets

Wealth tax is levied on the taxpayer's total net wealth as at 31.12 of the year in question, after social security deductions. It is therefore important to make a proper assessment of this.

In general, assets must be valued at market value. [Art.14 al.1 LHID] Market value means the price that would be obtained in the event of a sale under normal conditions.

However, cantons may depart from this valuation method and use the return value. The yield value is obtained by dividing the yield for a given period by a capitalisation rate.

The yield value is mainly used for buildings used for agricultural purposes. On the other hand, property that is not used for agricultural purposes cannot be valued solely on the basis of yield.

Determination of gross assets

Moveable assets

Certificate from your bank as at 31.12.

L’Administration Fédérale des Contributions publie chaque année les cours de chaque monnaie virtuelle d’une certaine envergure en rassemblant les données de plusieurs plateformes.

In the absence of a valuation price, the cryptocurrency in question must be declared at its initial purchase price converted into Swiss francs and not at the price on 31.12.

Ce genre de titres sont évalués à leur valeur boursière au 31.12.

Non-listed securities are valued according to the yield and intrinsic value of the company in question. In practice, the cantonal tax authorities refer to the valuation rules set out in CSI Circular No. 28. Special valuation rules apply to real estate companies.

The valuation of Swiss securities will be provided to you directly by the cantonal administration.

This type of security is treated in the same way as unlisted Swiss securities. The tax authorities must be provided with all the information they need to assess the company correctly, including balance sheets, profit and loss accounts, annexes and the purchase contract.

Vous pouvez cependant interroger l’administration fiscale en demandant un ruling.

Certificate from life insurance provider at 31.12.

At market value, i.e. resale value under normal conditions

A certificate signed by the person paying the benefit is sufficient.

Real estate assets

The tax value corresponds to the purchase price on the contract. Properties subject to usufruct are taxable with the usufructuary.

The tax value corresponds to the value retained by the tax authorities at the time of the event.

These types of property are valued taking into account the current value of the land, buildings and ancillary facilities.

Farm buildings

Properties used for farming and forestry, including the part used as the owner's home, are valued at their yield value.

Il convient de préciser que le Conseil Fédéral a publié le nouveau guide d’estimation de la valeur de rendement agricole entré en vigueur le 1er avril 2018.

Determining net assets

Wealth tax is levied on the taxpayer's total net wealth, which is made up as follows:

- Gross assets (furniture and real estate)

- Debt (mortgage, unsecured and private)

- Social deductions (depending on your situation)

- Net taxable wealth

Gross assets

All your movable and immovable property (see above) valued in accordance with the above as at 31.12. of the year in question.

Debts

Debts are deducted from gross assets.

En font partie :

- Les dettes chirographaires (dettes non garanties)

- Les dettes hypothécaires

- Les dettes privées justifiées

- Extracts from negative accounts

- Quittances d’intérêts

Les dettes peuvent seulement être déduite de la fortune. Elle sont effectivement dues par le contribuable.

The guarantees may only be deducted in the event of the ascertained insolvency of the principal debtor. If the guarantee is by several people the calculation is made on a pro rata basis.

Répartition des dettes géographiquement:

Persons who also own assets outside the canton of Geneva may deduct from their gross taxable assets only the portion proportional to the assets subject to tax in the canton.

Social deductions on wealth

CHF 82’200

Personne seule sans enfants à charge (Ex : célibataire, veuf, séparé de corps ou de fait ou divorcé)

CHF 164’400

CHF 41’100

Pour chaque enfant supplémentaire

Deduction for the self-employed and partnerships : Jusqu’à 500’000 CHF pour la moitié des éléments de fortune investis dans l’exploitation commerciale, artisanale ou industrielle du contribuable. Si associé d’une SNC : au prorata de sa participation.

Social security deductions on assets outside Switzerland

For taxpayers who, in addition to assets subject to tax in the canton, own assets outside the canton that are not subject to cantonal tax, the department allocates these deductions as follows proportionally assets subject to cantonal tax as a proportion of total assets.

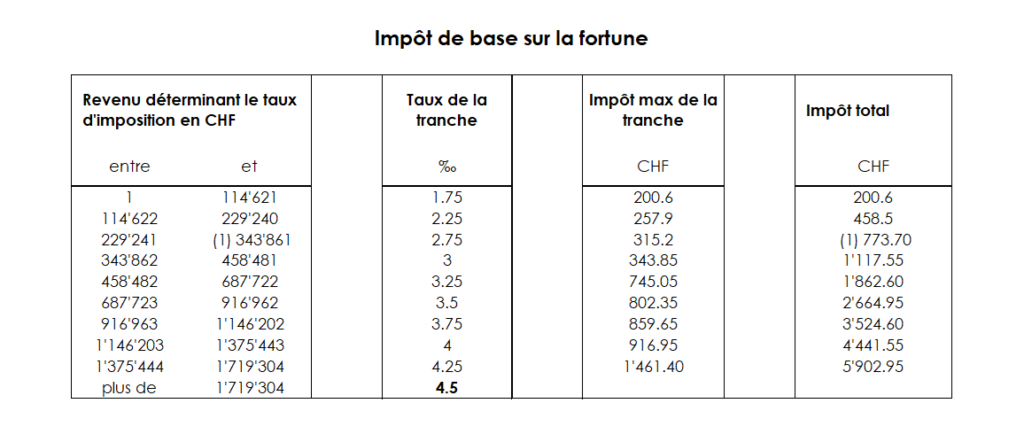

Wealth tax calculation and scales

Wealth tax is calculated in brackets that accumulate in stages.

Pour ce faire, il faut déterminer dans quelle tranche vous vous situez puis sur la différence entre le palier dépassé (complètement) et le palier final appliquer le taux de la tranche finale.

Exemple de calcul de l’impôt sur la fortune et de l’impôt supplémentaire pour l’année 2025

Calculation for a net worth of CHF 450,000 for a single person living in Geneva.

CHF 450’000

CHF 82’040

CHF 367’960

Calculation of basic tax

Tax for levels fully exceeded 338,033: CHF 760.55

(cumulative tax (197.20+253.50+309.85))

Tax on the balance at the following rate: CHF 89.80

(367,960-338,033 = 29'927 * 0.3%)

850.35 CHF

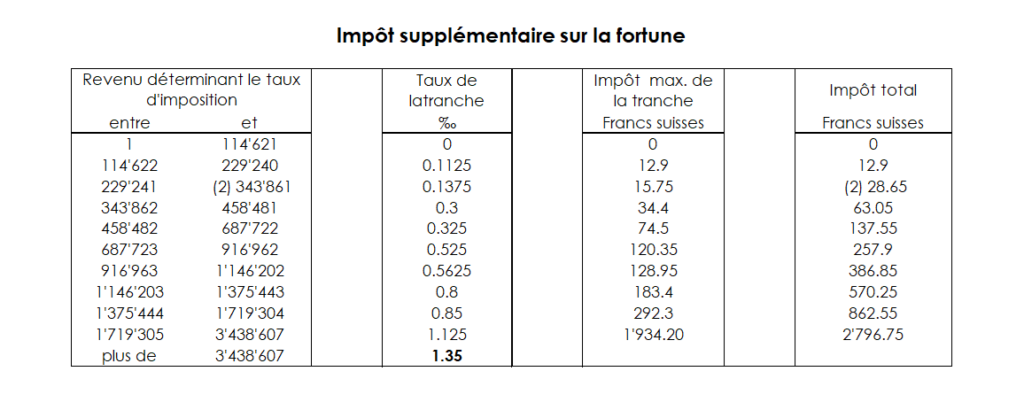

Calculation of supplementary wealth tax

Tax for levels fully exceeded 338,033: CHF 28.20

(Cumulative tax (12.70+15.70))

Tax on the balance at the following rate CHF 9.00

(367,960-338,033 = 29,927 * 0.03%)

Total impôt de base sur la fortune: 37.20 CHF

Pour le calcul des impôts additionnels cantonaux et communaux sur la fortune :

The basic tax determined below should be :

- add the cantonal additional centimes

- to add the additional cantonal centime to finance home help (1% of basic tax)

- to add the additional communal centimes (calculated on the basic tax)

Tax advice: wealth tax

In this article, we take a general look at the wealth tax system. The most important thing to remember is that wealth tax is levied by the cantons and municipalities, not by the federal government, and that it is important to declare your wealth fairly.

If you want to avoid the calculations mentioned in point 4 and leave this task to the specialists, don't hesitate to get in touch with us. If you have any questions or requests, please contact us via our contact form.